For new cardholders effective July 1, 2026, The Robinhood Gold Card FAQ was quietly revised to state a 3% foreign transaction fee “may be charged” when transacting in a foreign currency. Existing cardholders will retain the original 0% structure but not the new applicants after the cutoff date. This change was never disclosed via email or public announcement rather quitely inserted into an FAQ section titled “Do I Need To Provide A Travel Notice,” a location no cardholder monitors.

Robinhood Quietly Updated Its Gold Card Terms

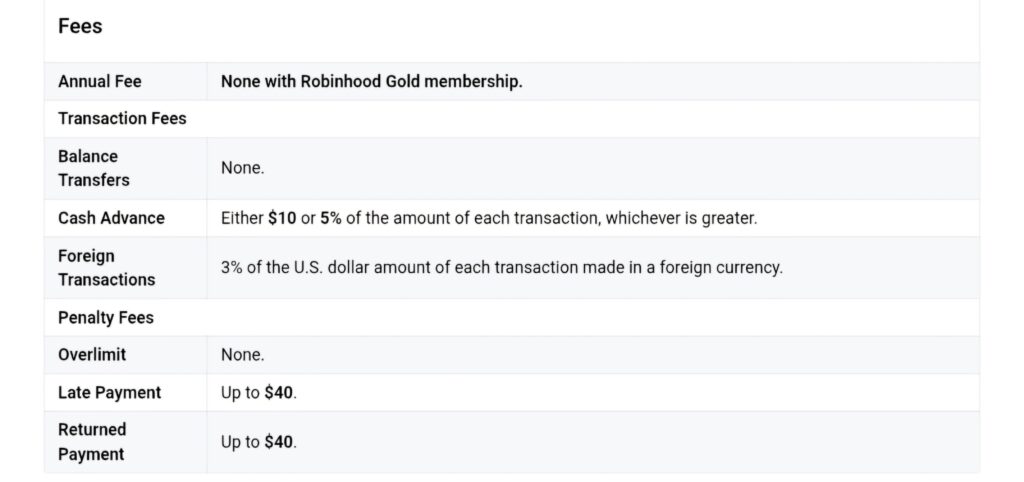

The official revised FAQ reads: “3% of the U.S. dollar amount of each transaction made in a foreign currency.” the exchange rate is based on Visa’s exchange rate calculator. This is a direct reversal of prior language. The earlier version stated the card “is available to be used internationally wherever VISA is accepted. There are no foreign transaction fees.” Both versions retained the Visa exchange rate calculator reference, but only one contained the fee. The insertion of a 3% surcharge is the material change.

We Have Proofs: The Wayback Machine Confirms the Fee Is New

Archived captures establish the timeline as of June 8, 2026 (that was when last crawled by Wayback Machine), the FAQ explicitly stated “There are no foreign transaction fees.”

For reference view the lastest Snapshots of Wayback Machine

The current version contains the 3% charge. This eliminates any ambiguity about whether the fee was always present and merely overlooked. It was added between early June and the July 1 effective date. Standard card overview pages still list the Robinhood Gold Card’s foreign transaction fee as “None.” That figure reflects the terms applicable to existing cardholders and pre July applicants. It does not reflect the new account policy. The discrepancy between marketing pages and the buried FAQ is the core friction point here.

Who Is Affected and Who Is Not

The fee applies to new users after July 1, 2026 as per Robinhood support. Existing cardholders are not currently charged the 3% FTF. Most major card issuers usually avoid adding foreign transaction fees to existing accounts once a card is marketed with 0% FTF, which is likely why current Robinhood Gold Card users appear to be grandfathered in for now. Still, Robinhood’s terms allow the company to change card benefits in the future with notice, so the current policy may not stay permanent. For new users, though, the impact is significant because the 3% fee effectively wipes out the card’s rewards value on purchases made in foreign currencies.

The card’s headline value is 3 points per $1 for Gold members. A 3% foreign transaction fee fully offsets that 3% earn rate. The effective net yield on international purchases drops to zero. For a user spending in foreign currency daily, the card’s primary advantage over competitors disappears entirely.

Is 3% Robinhood FTF a Problem, Answer is No but Why

Actually, main issue is not the fee alone. The blame goes to delivery method – No email, No statement notice. People just got compensated inside an FAQ subsection unrelated to fees. Usually, cardholders do not check FAQ pages weekly. This is functionally equivalent to reducing a rewards multiplier without disclosure. This type of step exposes a systemic risk in newer rewards products. The Robinhood Gold Card carries no annual fee on the card itself but the $50 cost on other side to use and keep the card is a must pay.

Well, technically we cant fully blame them for this because low cost & aggressive earn cards are structurally vulnerable to unannounced revisions due to the thin margins issuer has.

So, stop worrying much about 3% incase you got hit, as there are more issues to lookat, like the additional friction points which already exist: cases have been seen where rewards are reduced if Robinhood flags a spend pattern as resale or commercial use and third party bill pay including rent and taxes is excluded from earning.

Here is the direct link to their Official Webpage incase you weren’t able to find official documents, else check the latest copy of live screenshot to save time.

Should You Still Use the Robinhood Gold Card Abroad

Verify status first. If the account was opened before July 1, 2026, the 0% FTF currently holds. Test with a small foreign currency transaction and confirm no 3% fee posts to the statement before relying on the card abroad.

Better Credit Cards for International Spending

For anyone opening a new account or living abroad, the Gold Card is no longer a good choice for international spend. Multiple competitors charge no foreign transaction fee and are backed by established issuers with more predictable terms, like these cards –

| Credit Card | Annual Fee | FTF Fee | Base Reward Rate |

| Robinhood Gold Card | $50 (via Gold Subscription) | 3% | 3 points per $1 (Gold member) 1.5 points per $1 (non-Gold) |

| Capital One Venture Reward | 95$ | 0 | Unlimited 2x miles per $1 |

| Capital One Venture X Rewards | 395$ | 0 | Unlimited 2X miles per $1 |

| American Express Platinum | 895$ | 0 | 1X points per $1 (5X on select travel) |

| Chase Sapphire Preferred | 95$ | 0 | 1x on general purchases (upto 5x on select category) |

None of these carry a 3% surcharge on foreign transactions. The advice for international spenders is clear: do not rely on a card whose fee structure was altered without notice. Confirm your grandfathered status if you hold the card, and route foreign currency purchases to a card with a durable 0% FTF policy from an issuer with a longer track record.